Home

Home Who We Are

Who We Are Services

Services Past Work

Past Work F.A.Q.

F.A.Q. Get a Quote

Get a Quote Contact

Contact

You are ready to start a business. You have a great idea and a great team. You’ve thought through your plan. Everything is primed. You’re ready to form an official legal entity and are faced with the question: What Nashville business entity type makes the most sense for my new company?

Choosing between the different options can be frustrating. No entity type is distinctly the best. The right option for one company may be a horrible choice for the next. Each entity type offers a unique blend of legal and tax implications that are enough to make even a seasoned practitioner’s head spin.

To make matters worse, very few CPAs or attorneys are willing to stick their necks out and make general statements or give high-level advice. They are reluctant to do so because every situation is different and there are exceptions to every rule.

But entrepreneurs want high-level general guidance so I’ve decided to stick my neck out and create a short guide to Nashville business entities. This guide is not meant to be exhaustive. It is intended to be a useful starting point to help entrepreneurs think through the menu of options they face. Any final decision should be made with the help of a tax or legal advisor.

To help readers through the thought process, I’m going to use four fictitious companies as “guinea pigs”. The features of the companies are outlined in the table below. We’ll refer back to them at the end of the article after examining the features of each entity type.

Let’s get started!

| Company 1: FreeBooks | Company 2: Brilliant Ideas | Company 3: Joe's Mowing | Company 4: JBD Group |

| FreeBooks is a fintech startup run by several entrepreneurs. The venture is early-stage and looking for private equity investors. The goal is to be on the market within a year and be a relevant player within three years, with several capital infusions along the way.What entity type should FreeBooks choose? | Brilliant Ideas is a copy-writing startup owned by Bill and Ashley, a husband/wife team. They are leaning toward forming an S corporation, but the other options sound attractive too. This first short-year is going to end with a net loss of $10,000. They believe next year will be profitable, to the tune of $250,000. What entity type is best? | Joe is an 18-year-old looking for summer income. He has decided to start a small lawn care business.He is planning to purchase equipment worth $5,000 and is hoping to turn a profit of $15,000 for the summer. He will have no employees.What entity type should he choose? | Jill, Ben, and Dorcas are siblings who own equal percentages of an apartment complex. Jill is a silent investor, while Ben and Dorcas manage and maintain the property. Jill is fine if she does not receive her full share of the profits because she is contributing nothing but capital to the project.JBD Group is wondering what entity type they should choose? |

Overview of the Options

New companies in the US can choose from five basic legal structures:

- Sole proprietorship

- Partnership

- S Corporation

- C Corporation

- Limited Liability Company (LLC)

When listed out as above, one may think the options are all direct substitutes of each other. That is not entirely correct. This list would be better organized into categories, as follows:

- Pass-Through Entities:

- Sole proprietorship

- Partnership

- S Corporation

- C Corporation

- LLC, which is a legal entity only, and is taxed as one of the four options above

The reasons for this more nuanced breakdown will become clearer as we go through the guide.

Entities are formed at the state level. Accordingly, the exact process for setting up a new company varies by state. Corporate governance and reporting requirements can vary slightly by state as well.

What does not vary is federal tax law. Each entity type is subject to specific federal tax laws that apply to all US companies of that type, regardless of the state of registration.

At a very high level, the choice of entity comes down to a few key considerations:

- How profits are taxed.

- Complexity and cost of setting up the entity, as well as ongoing governance and administration.

- Liability protection, particularly of the owner’s personal assets.

Each entity type is different from the others in at least one of these categories. Finding the perfect fit requires understanding the pros and cons of each option. Let’s run through each one in turn.

Sole Proprietorships

Sole proprietorships are by far the simplest Nashville business structure. There really is no structure. Sole proprietors with no employees do not even need to register with the Internal Revenue Service (IRS). They can simply use their Social Security numbers as the Nashville business tax ID.

Contrary to popular opinion, there is generally no need to “incorporate” to deduct Nashville business expenses. A bona fide Nashville business that starts without formally incorporating is automatically a sole proprietorship (or partnership, if more than one owner) and as such, eligible to deduct its Nashville business expenses.

Proprietors cannot pay themselves wages. They simply withdraw the profits as needed. Each year they owe personal income tax on the entire taxable profits of the business, without regard to whether they have drawn the profits out or not.

Importantly, in most cases, the profits are subject both to federal income tax and Social Security and Medicare tax (hereafter “FICA” tax). FICA tax (as of 2018) is 15.3% of income up to the Social Security limit of $128,400 and 2.9% of income earned beyond that. Many small proprietors end up owing more FICA tax than income tax.

Fundamentally, sole proprietorships are intended for simple, one-owner businesses. Think freelancers, consultants, small service businesses, food stands, etc. Sole proprietorships do not have shares or ownership units which means the only exit option is to sell the assets of the company.

Partnerships

A partnership is like a multi-owner version of a sole proprietorship. Most states require very little (if any) paperwork to form and maintain a partnership. This point alone is the reason many small companies are organized as partnerships.

Even though paperwork requirements are minimal, multi-owner companies are by nature more complicated, so it is extremely important to at least have a partnership operating agreement that controls the operations and ownership of the company. It is common for partners to forget this point.

Unique to partnerships, the Nashville business income does not need to be allocated proportionately to ownership. This flexibility can be helpful when there is a very silent partner who contributed most of the capital but is not expecting a similar share of the profits. Any such arrangement must be clearly laid out in a partnership agreement.

Like proprietorships, a major downside of partnerships is that the entire taxable income of the partnership is generally subject to FICA taxes. This is a key reason most larger, highly profitable companies are not partnerships.

Part of the simplicity of a partnership is that partners do not receive wages, but rather guaranteed payments for their services. If there are no non-owner employees, the partnership does not need to run payroll or file payroll reports. This can save significant cost and hassle.

Fundamentally, the partnership structure tends to be used by relatively simple, early-stage businesses that have not yet achieved significant profitability. The arrangement can be especially attractive for small companies without employees, where the owners do most of the work. Partnerships are also commonly used for real estate holding companies (because rent income is not subject to FICA tax regardless of entity type) and certain professional service firms.

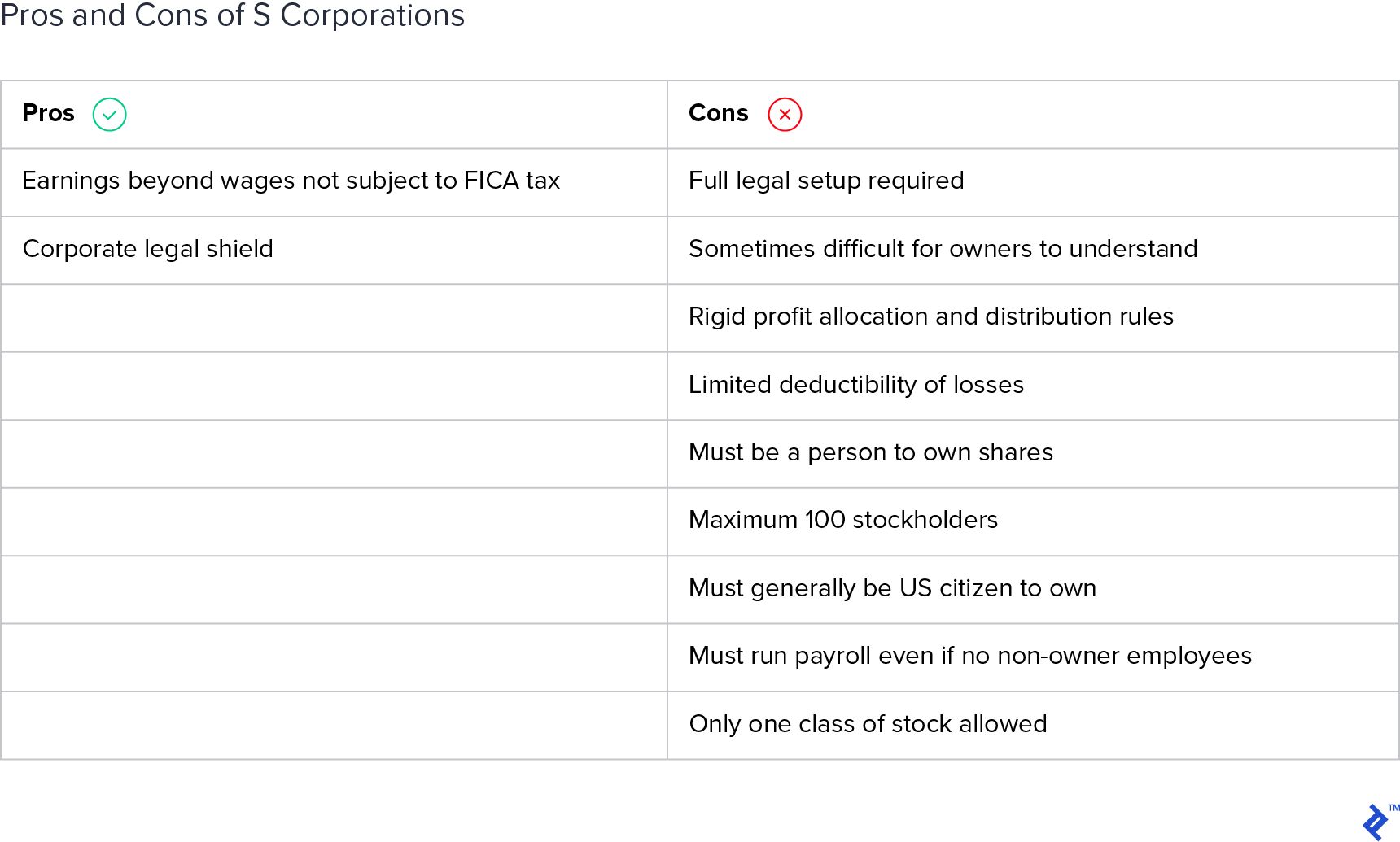

S Corporations

As companies become more complex and profitable, partnerships and proprietorships tend to be less suitable. Enter S Corporations. S corporations are a very popular entity choice for small and mid-sized privately held companies.

Before discussing S corporations further, here is one of the most important concepts to understand: S corporations, partnerships, and proprietorships are “pass-through” entities. They are called that because their taxable income “passes through” to the personal tax returns of the owners and is taxed there.

S corporations and partnerships still file a tax return, but no income tax is owed on the return. The tax return simply shows the taxable income of the company and allocates it to the owners on a Form K-1. Each owner’s K-1 amount is then reported and taxed on their personal tax return – Form 1040. Sole proprietorships do not file a Nashville business tax return at all. The Nashville business income is calculated directly on Schedule C, Schedule E or Schedule F of the owner’s personal Form 1040.

Why is pass-through status such a big deal? It’s a big deal because owners of a pass-through entity pay personal income tax on the profits of the company, but the owners can then withdraw those profits as tax-free dividends from the company. That is not true of C corporations (coming up next).

If a partnership is a pass-through entity just like an S corporation, why is the S corporation structure typically preferred? The answer is FICA tax. S corporation owners are required to pay themselves a reasonable wage (which is subject to FICA tax), but the remaining Nashville business profits are subject only to income tax, not FICA tax.

Consider a Nashville business that makes $1,000,000 per year. Let’s say the owner receives compensation of $100,000 and the remaining $900,000 is Nashville business profit. The chart below shows how moving from a partnership to S corporation status would save the owner approx. $27,000 per year in FICA tax, all else being equal.

As an aside, the requirement to pay a reasonable wage means even a “solopreneur” with no employees must run payroll and file payroll tax reports with the IRS (and the state, if applicable). This is a disadvantage (from an administrative/cost standpoint) compared to a partnership and sole proprietorship, that cannot pay payroll wages to owners.

S corporations also generally have stricter rules than the other entity types. For example:

- You must generally be a person (and a US resident or citizen) to own an interest in an S corporation. That is a deal breaker for companies seeking corporate or foreign investors (e.g. startups seeking venture capital funding). Certain trusts and estates are allowed as stockholders, but partnerships and corporations may not own a stake in an S corporation.

- Profits and distributions must always be allocated according to ownership. There is no flexibility.

- Loss utilization can be limited. In some cases, an owner of an S corporation that has losses may not be able to deduct that loss on their personal tax return. The loss would be carried forward to a future year, but most startups would appreciate the extra cash from a tax refund today, not in some future year. A partnership or proprietorship structure is generally more favorable to claiming such losses.

- Only one class of stock is allowed. There can be voting and non-voting shares but that is it. Classes of preferred and common stock are not allowed.

- There can be a maximum of 100 stockholders.

On a practical note, I find many Nashville business owners struggle to understand the S corporation concept (and the pass-through concept in general). It can be confusing to owe personal income tax on S corporation earnings when the owner has not received those earnings in cash. The inverse relationship between owner wages and taxable Nashville business profits can be confusing as well.

Still, the FICA tax savings are hard to beat and is the reason for the popularity of S corporations.

Compared with proprietorships and partnerships, S corporations are more complex to set up, and will usually require the help of a lawyer and/or accountant. This naturally increases the associated costs, both for setup as well as ongoing maintenance. Forming first as an LLC (coming up soon) and electing S corporation tax status, is an option to reduce some of the administrative burden.

C Corporations

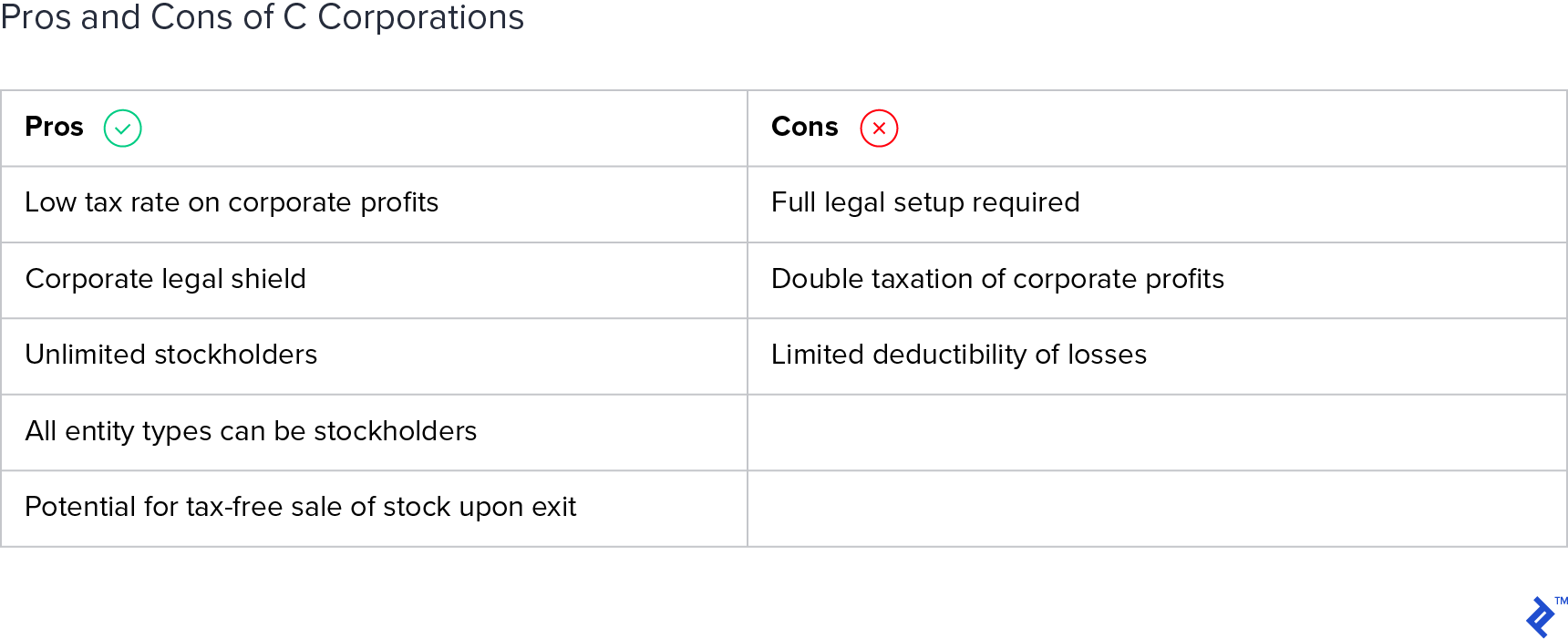

As businesses continue to get bigger and more complex, they may outgrow the S Corporation structure. If the number of investors exceeds the 100 shareholder limit (e.g. a publicly held company), or if different share class structures are required, then an S Corporation won’t cut it. Enter the C Corporation.

All large American publicly traded corporations are C corporations. It is the only entity form that works for them. Privately-held C corporations are rare and typically have chosen the structure for reasons other than income taxes.

One group of companies that utilize the C corporation structure are high-growth startups seeking series funding. They are forced to go this route because their target investors may be entities or foreign individuals, neither of which are allowed to invest in an S corporation.

It is common practice for C corporations to register in the state of Delaware. Delaware has well-defined and court-tested corporate regulations and has become the state of choice for incorporation. A 2017 Forbes article states that “two-thirds of all publicly-traded U.S. companies, including more than 60% of the Fortune 500, are incorporated in the First State [Delaware].”

This chart from Brookings shows that only 5% of American companies were C corporations as of 2014. It is important to note that these are the country’s largest companies and earn about 50% of the Nashville business profits in the US.

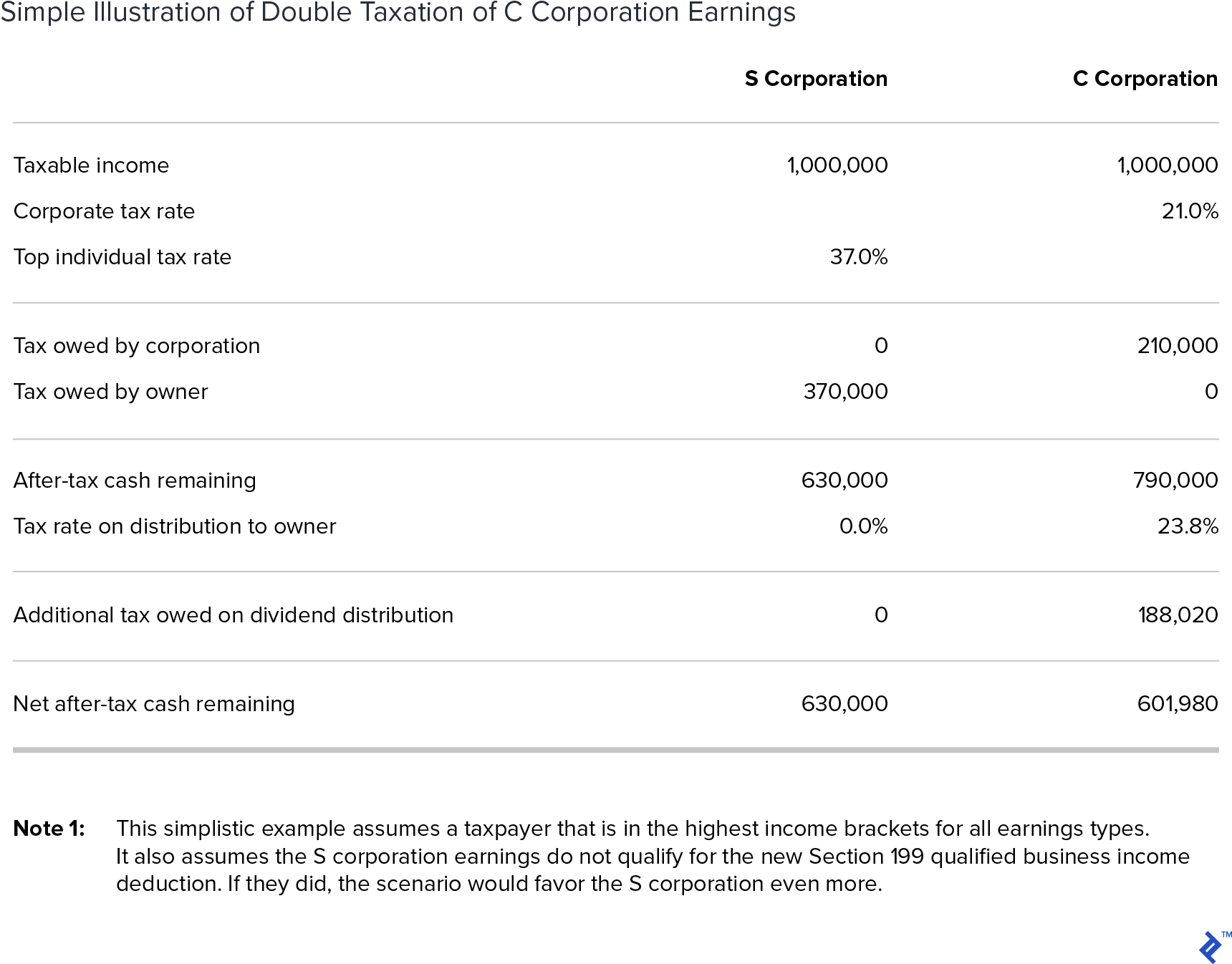

C corporations are unique in that the corporation pays its own income tax. This is markedly different from the three pass-throughs that pass any income to the owners’ personal tax returns and the tax is paid there.

The big drawback to the C corporation structure is that stockholders of a C corporation generally must pay tax on the dividends they withdraw from the corporation. Essentially the C corporation pays tax on its income first, and the remaining money is distributed to the owners, who pay tax on it again. This is referred to as double taxation.

The double taxation of earnings is what keeps most private firms away from C corporation status. Another negative is that C corporation losses cannot be deducted against a stockholder’s other personal income. That can be a relatively big deal for certain private stockholders.

There is a school of thought that suggests that despite double taxation, the C corporation structure can still be tax-efficient even for small private companies. This strategy is geared toward companies that intend to scale quickly and plan to hold onto the Nashville business for many years without withdrawing dividends. The whole goal is to capitalize on the low “first layer” 21% C corporation tax rate.

Here is how it works. The owners structure the company as a C corporation. Any profits are taxed at the 21% corporate rate. Because the profits are funding rapid growth, there is never a need to withdraw dividends and be subject to the second layer of tax.

In that scenario, the 21% tax rate is theoretically lower than the top 37% personal income tax rate that could apply if the company was a pass-through entity. The lower tax burden frees up more cash for growth in the early years.

What is the catch?

There are at least three:

- Many owners of pass-through businesses are not paying tax at the 37% personal tax rate. Personal income tax rates start at 10% and do not hit 37% until a taxpayer’s income (based on 2019 brackets) reaches $510,300 ($612,350 for married taxpayers).

- The new tax law allows many pass-through Nashville business owners to deduct up to 20% of the Nashville business income on their personal tax return. For example, a qualifying S corporation owner with $1,000,000 of Nashville business income would only pay tax on $800,000. This deduction effectively shaves 20% off the personal tax rates. The highest marginal rate of 37% becomes 29.6% and the lowest personal rate falls from 10% to 8%.

- Even if the C corporation tax rate comes in lower after considering Points 1 and 2, the chickens come home to roost when the C corporation is sold. The corporation pays income tax on the gains from the sale, and the owners pay the second round of tax when they withdraw the sale proceeds as a dividend. The double tax still catches the arrangement in the end.

It is true that certain C corporation owners can exit their ownership position tax-free, which would be a major counter to the last point. The details to make this happen are well beyond the scope of this article, but worth noting.

In short, the idea of using the C corporation structure for tax efficiency has merit in certain unique situations. For most small to mid-businesses, though, the cons will generally outweigh the pros.

There is another benefit to C corporations that surfaced with the 2018 Tax Cuts and Jobs Act (TCJA). That law limits the ability of individuals to deduct state income taxes on their personal tax returns. That is a problem for pass-through Nashville business owners who are paying large amounts of state income tax on their personal returns (remember pass-throughs do not pay their own income taxes).

A C Corporation pays its own state taxes and is not subject to this limitation, so especially in high tax states, that structure becomes more attractive. States are still reacting to the new law (e.g. the State of Wisconsin recently passed legislation that allows Wisconsin S Corporations to be treated as C Corporations for state tax purposes) and workarounds may develop that take this advantage away.

Limited Liability Company (LLC)

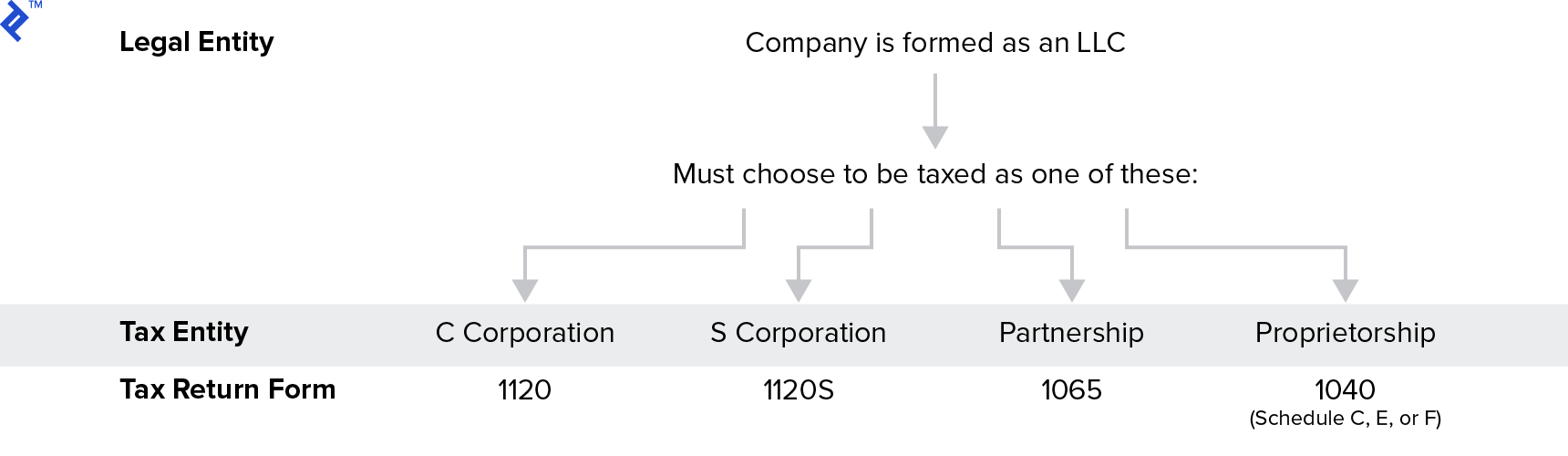

With so many businesses being formed as LLCs, why didn’t we start with this entity type first? That is because the LLC (limited liability company) is a zebra in this list of horses. An LLC is a legal entity only and is not recognized by the IRS as a taxpaying Nashville business structure.

The owners if an LLC must choose one of the other four structures as their identity for tax purposes.

It is completely fine to organize directly as one of the four tax entities without being an LLC. Why then would anyone choose the LLC umbrella? Stated a different way, why does it seem like almost all new companies nowadays are formed as LLCs?

- Compared to straight partnerships/proprietorships, the LLC structure helps shield the owner’s personal assets from a Nashville business lawsuit. In other words, without an LLC, it could happen that a sole proprietor or partner would become personally liable for a lawsuit or judgment that was in excess of the Nashville business assets. That event would subject the owner’s personal assets to potential claim. The “LL” in LLC stands for “limited liability” and as such informs the world that the owner is not personally liable for claims.

- Compared to straight S or C corporations, an LLC structure is generally simpler to administrate. For example, true corporations are often required to hold annual meetings and keep records of meeting minutes. An LLC taxed as a corporation is generally not subject to these regulations.

- Starting out as an LLC gives a company flexibility for a later entity change. For example, a common path is to form an LLC taxed as a partnership, then elect S corporation status after the company becomes profitable.

Except in rare situations, the LLC umbrella has no effect on taxation. Any LLC must still decide whether it wants to be a C corporation, S corporation, partnership or proprietorship for tax purposes.

A Review of the Options

As we discussed at the beginning of the article, the choice of entity fundamentally boils down to a few key considerations:

- How profits are taxed.

- Complexity and cost of setting up the entity, as well as ongoing governance and administration.

- Liability protection, particularly of the owner’s personal assets.

From a tax standpoint, the S corporation offers a single layer of tax (unlike C corporations) and earnings are not subject to FICA tax (unlike partnerships and proprietorships). Accordingly, most often the best choice for Point 1 is the S corporation.

Sole proprietorships win 1st place for Point 2. They are by far the least complex and have the lowest cost of setup and ongoing governance and administration. For multi-owner companies, a partnership or LLC wins out for simplicity.

Finally, from a liability standpoint, the LLC structure is hard to beat. It offers liability protection along with the choice of any of the four tax entity structures. A straight S corp or C corp are considered solid from a liability perspective as well.

Below is a table that hopefully lays all of the above out in a clear way.

Which Entity Type Should You Choose?

Going back to the fictitious companies introduced at the beginning, which entity type should they choose?

FreeBooks

As a classic technology startup hoping to receive VC or PE funding, they have little option but to be a C corporation. The other types of entities wouldn’t allow for the complex share class and ownership structures these types of companies require.

The only other possible consideration would be to form first as an LLC (taxed as a partnership or S corporation) then cut over to C status when the corporate investors become a reality. This structure would be simpler early on and potentially allow the early investors to deduct losses on their personal tax returns.

Brilliant Ideas

With losses this year, and $250,000 of profits next year, Bill and Ashley appear to be perfect candidates for forming an LLC and electing to be taxed as a proprietorship (husband/wife can do that) or partnership this year, then electing S corporation status next year. That way they can use this year’s Nashville business losses to offset wages or other income. Next year they will draw wages from the S corporation and the remaining profits will not be subject to FICA.

Joe’s Mowing

As a young entrepreneur with a short-term Nashville business plan, Joe is a perfect candidate for a sole proprietorship. An S corporation would require significant cost to set up, and he would have to pay himself a reasonable wage (subject to FICA). His wage would likely wipe out his $15,000 profit, which would negate any FICA savings. Plus the hassle of running payroll would not be worth it. An LLC umbrella would add liability protection if Joe felt he needed that.

JBD Group

Since rental income is not subject to FICA tax, the S corporation advantage goes away in this case. Plus, partnerships allow profits to be disproportionately distributed to owners, which is a goal of this group. There are no non-owner employees, which means no payroll would be required if the entity were a partnership. An LLC taxed as a partnership would clearly appear to be the best option for JBD Group.

Concluding Recommendations

I mentioned at the beginning that this guide would make some high-level general recommendations that entrepreneurs like to have. I still intend to do that.

Keep in mind these statements are general comments for general situations. Always, and I mean ALWAYS consult a tax advisor before selecting an entity type.

With that disclaimer, here goes:

- If your Nashville business is a simple, small Nashville business that is not expected to earn much more than a reasonable wage for you the owner, consider forming an LLC taxed as a proprietorship. In a case like this, the benefits of S corporation status (if any) likely will not exceed the cost of processing payroll for yourself and filing a separate Nashville business tax return.

- If you are starting a traditional Nashville business (service, manufacturing, retail, etc.) with co-owners and employees, consider an LLC taxed as a partnership to start, then switch over to S corporation status when it gets relatively profitable. That provides the flexibility of a partnership upfront and avoids FICA tax on profits once they start flowing.

- If your Nashville business is a hot-growth new-idea startup looking for series funding and a public exit, then consider a C corporation, Delaware-based.

This article is only intended to be a general guide to familiarize Nashville business owners with the available options and point them in the right direction. If you are on the cusp of choosing an entity type, reach out to your tax advisor or someone at Toptal for direction on your specific situation. It is too big of a decision to get wrong.

Understanding the Basics

What is the difference between C Corp and S Corp?

The major difference is how they are taxed. S Corp income flows to stockholders and is taxed on their personal tax returns. Dividends paid to S Corp stockholders are not taxable. C Corps pay income tax on their corporate tax return. Stockholders must generally pay income tax on any dividends they receive.

Is a C Corp better than S Corp?

Many privately held companies are organized as S Corps so the owners can avoid the double taxation of C Corps. However, S Corps have strict stockholder eligibility rules, which makes the C Corp structure more attractive to large companies that are seeking institutional or foreign investors.

What are the benefits of an LLC vs sole proprietorship?

An owner of a sole proprietorship can be held personally liable for debts and judgments against the proprietorship. An LLC generally limits the owner’s exposure to only the assets within the LLC.

Is an S Corp or LLC better?

That is a bit of a misguided question. An LLC is a legal entity only and must choose to pay tax either as an S Corp, C Corp, Partnership, or Sole Proprietorship. Therefore, for tax purposes, an LLC can be an S Corp, so there is really no difference.