Picture this: You find the perfect home in East Nashville listed at $500,000. You're excited and ready to make an offer.

At a 3% rate (what buyers got in 2021) and with a 20% down payment, your monthly payment—for principal and interest only—would be around $1,686. At a 6.3% rate today? That same house costs you $2,476 per month in interest and principal. That's around $790 more every single month for the exact same home.

Interest rates change what you can afford, how much competition you face, and whether you should buy or sell right now. When you’re researching the market, understanding these changes could save you tens of thousands of dollars.

Here's what you need to know about how interest rates are shaping Nashville real estate in 2026.

For informational purposes only. Always consult with a licensed mortgage or home loan professional before proceeding with any real estate transaction.

Quick Takeaways: What Interest Rates Mean for You

If you're buying in Nashville:

- Current 6–6.5% rates reduce your buying power by around 30% compared to 2021

- Waiting for rates to drop could cost you more, as home prices keep rising annually

- Rate buydowns and seller credits can offset higher rates

- Government-backed loans (which typically have lower rates than conventional) now offer higher limits: FHA up to $943K, VA up to $989K

If you're selling in Nashville:

- Higher rates mean fewer buyers, but inventory is still tight in many areas

- Competitive pricing matters more now than in 2021–2022's seller's market

- Offering buyer incentives like closing cost help or rate buydowns attracts more offers

- Your home equity can help offset the higher rate on your next purchase

Nashville Mortgage Rates in 2026: Where We Stand

Right now, the national average 30-year fixed-rate mortgage APR is around 6.3%. That's where it’s settled after a wild few years, and mortgage rate forecasts are predicting that they’ll stay in the low 6% range for a while. Maybe dip ever-so-slightly below.

Back in 2020 and 2021, rates dropped below 3%. The pandemic pushed the Federal Reserve to keep rates incredibly low. Homebuyers could borrow money cheaper than ever before. That created a buying frenzy and a strong seller’s market—bidding wars, homes selling in days, prices shooting up fast.

Then inflation hit hard in 2022. The Federal Reserve raised rates to cool down the economy. By late 2023, mortgage rates peaked above 7%. Buyers pulled back. The market slowed down.

Now, at the start of 2026, rates have stabilized. Buyers and sellers are starting to accept these rates as the new reality. People waited through 2023 and 2024, hoping for big drops. That didn't happen. And it probably won't.

The Federal Reserve has signaled it might make small rate cuts, but mortgage rates don't automatically follow. Any decline will be slow and gradual.

Experts predict rates will dip in 2026, but only slightly—perhaps averages in the 5.5–6% range. Returning to 3–4% rates won’t happen anytime soon.

What does this mean for Nashville? Buyers need to budget based on today’s rates, not hope for yesterday's rates. Sellers need to understand that buyers face higher monthly payments, which changes negotiation dynamics.

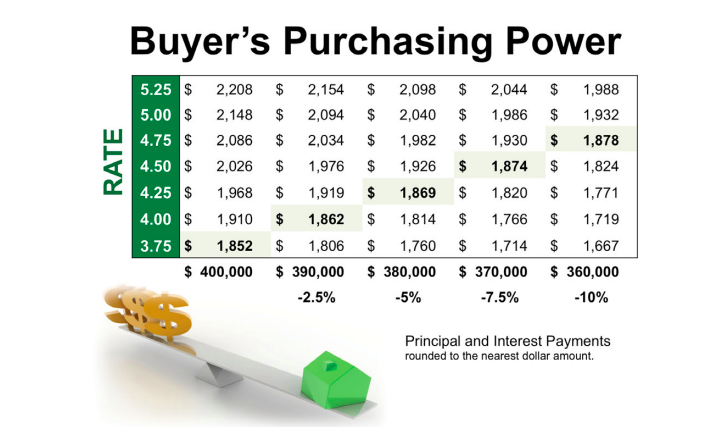

What a 6.3% Rate Really Costs Nashville Buyers

Let's look at real numbers using a $500,000 house and a 20% down payment (total mortgage amount: $400,000). For this comparison, we’re only looking at principal and interest, not home insurance or property taxes.

At 3% (what buyers got in 2021):

- Monthly payment: $1,686.42

- Total interest paid over 30 years: $207,109.81

At 6.3% (typical rate in 2025):

- Monthly payment: $2,475.89

- Total interest paid over 30 years: $491,320.82

That's $789.47 more every month. Over the life of the loan, you’ll pay an additional $284,211.01 in interest.

Here's another way to think about it: you qualified for a $400,000 mortgage at 3% in 2021 but decided the timing wasn’t right. Now you want to pull the trigger, but you’re aiming for the same mortgage payment that the 2021 numbers would’ve gotten you.

At a 6.3% interest rate, you’d be limited to a mortgage amount of around $272,000. The houses you’re looking at? Around $340,000. In effect, you lost $160,000 in buying power.

This is the 1/10 rule of interest rates: for every 1% change in interest rate, you can expect to change your homebuying budget by around 10%.

The income requirements changed dramatically as well. Experts recommend spending only up to 28% of your income on housing expenses.

Including estimated property taxes and home insurance on a $500,000 property in Nashville, you’d need an annual income of around $127,600 to afford the home at 6.3%. In 2021, at 3%, you needed about $93,700.

The Real Cost of Sitting on the Sidelines in Nashville

You might be thinking: "I'll just wait until rates drop to 5% or lower."

Here's why that could backfire.

Nashville has a ton of pent-up housing demand. Thousands of people delayed buying over the past two years, waiting for better rates. They're all sitting on the sidelines with you.

When rates DO drop—even to 6%—all those buyers will jump into the market at once. More buyers mean more competition. More competition drives up prices fast.

The Math on Waiting

Let's say you plan to wait a year, hoping rates drop from 6.3% to 5.5%. That would save you about $205 per month on a $400,000 mortgage.

But prices won’t stay steady during that time.Nashville home prices are projected to increase 2–4% in 2026. If you're looking at that $500,000 home today, it could cost $510,000 to $520,000 next year.

Home appreciation erodes your interest savings. Today, your monthly payment would be $2,475.89. Next year, best-case scenario, it would be $2,316.58—a savings of about $159, not $205.

And that’s if interest rates drop that low. If, as some experts forecast, the interest rate remains steady throughout 2026, you may be looking at a payment of around $2,575 next year, costing you an extra $100 per month instead.

Plus, while you wait, you're paying rent instead of building equity. Every month of rent is money you'll never get back. Meanwhile, homeowners are building wealth through appreciation.

Remember, you can start building equity now and refinance your mortgage if rates drop. If rates drop 1%, the savings generally offset the closing costs of the refi. (But always calculate for your own situation.)

Nashville's Job Market Fuels Demand

Amazon and Oracle are expanding their Nashville offices in 2026. Healthcare continues to grow. The entertainment industry brings steady employment. Nashville's unemployment rate sits at around 3%, well below the national average.

Strong job growth means people keep moving here. That keeps housing demand high. If you’re waiting for some dramatic market crash or price drop, Nashville's economic fundamentals don't support that scenario.

How to Buy Smart When Nashville Rates Aren't Budging

Higher rates don't mean you can't buy. They mean you need smarter strategies.

Negotiate Rate Buydowns from Sellers

This is huge right now. In early 2025, Redfin reported near-record highs of home sales with seller concessions nationwide (around 44%). Seller concessions remained a popular negotiating tactic through the housing market we’ve seen last year. These concessions, when offered, are often 1–3% of the home price.

You can use these credits to "buy down" your interest rate. Essentially, you pay money up front to permanently lower your rate—1% of the mortgage amount equals a 0.25% lower rate.

It’s important to calculate the breakeven point of buying points and evaluate how long you plan to stay in the home. But if you’re buying for the long term, points can save you far more than they cost.

You can also take the out-of-pocket money you save from seller concessions and apply it to your down payment. Smaller loan, smaller monthly payments. It’s worth it to run the math to find your best option.

Ask your agent to negotiate seller credits into your offer. In today's more balanced market, sellers are often willing to help.

Consider Adjustable-Rate Mortgages

ARMs offer lower rates for the first 3, 5, or 7 years, then adjust based on market conditions. If you plan to sell or refinance within 5 years, a 5/1 ARM at 5.5% beats a 30-year fixed at 6.5%.

The risk is that if rates stay high and you don't sell, you could end up paying more later. But if rates drop, you can refinance into a fixed-rate loan. Many Nashville buyers are using ARMs as a bridge strategy.

Shop Different Nashville Neighborhoods

Your budget stretches differently across Middle Tennessee:

Rutherford County offers median prices around $424,000. That's roughly $50,000 less than Nashville. Remote work makes the commute less painful for many buyers.

Sumner County averages around $439,000—a middle ground between affordability and proximity to downtown Nashville.

East Nashville, The Nations, and Wedgewood-Houston offer appreciation potential if you can afford Davidson County prices. These neighborhoods are expected to outperform citywide averages.

Williamson County commands premium prices near $928,000 (not surprising with expensive towns like Franklin and Brentwood), but inventory stays tighter there.

Look for areas with 4–6 months of inventory. More supply gives you negotiating leverage even when rates are higher.

Use Government-Backed Loans

Loan limits increased for 2025:

FHA loans in the Nashville metro now go up to $943,000 for single-family homes. You can put down as little as 3.5% with a credit score of 580 (or 10% down with scores as low as 500).

VA loans for veterans and military families now allow up to $989,000 with zero down payment in Davidson County.

USDA loans are available in outlying suburbs and rural areas, offering 100% financing to eligible buyers with moderate incomes.

These programs make homeownership possible for many buyers even when rates are higher and homes cost more. Because these loans are guaranteed by the government, they're less risky for lenders—and less risk translates into lower interest rates.

Improve Your Credit Score

Even small improvements to your credit score matter. Lenders group their rate tiers in brackets, not by every single point. Moving from a 718 to a 720 credit score might bump you up a tier and drop your rate by 0.125% or more. (Lender pricing matrices vary, but that’s a common average tier change.) That saves around $32 per month on a $400,000 loan. Over 30 years, that's around $11,600.

Check your credit report for errors. Pay down credit card balances below 30% of your limit. Set up autopay. Don't open new credit accounts while mortgage shopping. Give yourself 3–6 months to boost your credit score before applying.

Save a Larger Down Payment

20% down eliminates private mortgage insurance (PMI), which can cost 0.3–1.5% of your loan every year. That helps offset higher interest costs.

Plus, a larger down payment often gets you a slightly better rate from lenders.

Selling Your Nashville Home? Rates Change Your Strategy

If you're selling, higher rates affect you differently than buyers—but they still matter.

The Rate Lock-In Effect

As of late 2025, about 54% of U.S. homeowners still have locked-in mortgage rates under 4%. Maybe you're one of them. The idea of selling your 3.5% mortgage and getting a new one at 6% feels painful.

These “golden handcuffs” have put a squeeze on inventory for years. Instead of trading up or downsizing and listing their old homes for sale, homeowners have been staying put. While the percentage of homeowners with these historically low rates has been slowly decreasing as life events force sales, it’s still locking up a significant number of houses.

But here's what sellers forget: your home equity.

Let's say you bought in 2020 for $350,000 at 3%. Your home is now worth $490,000. You have $140,000 in equity (plus whatever you paid down on the principal).

Have your sights on a $500,000 home? A 20% down payment costs just $100,000 of that equity—with nothing out of your savings account. And you still have profit left over to invest, buy points, or apply toward principal.

You're not losing your low rate—you're using the wealth it helped you build. Your equity enables you to relocate for a better-paying job, move somewhere you’ve always wanted to live, or buy a house that better suits your needs.

2026 Nashville Selling Reality

The Nashville real estate market has changed. It's no longer the crazy seller's market of 2021–2022.

Inventory is up around 16% year-over-year in Nashville proper. More homes are sitting on the market longer. The average days on market is over a month.

Homes are selling closer to list price—or below it. Price reductions are becoming more common. Nationally, over 25% of listings have been getting price cuts in recent months. Nashville isn't immune.

What does this mean? Pricing strategy matters more now. You can't overprice and expect bidding wars to bail you out. Buyers are more cautious. They're comparing options carefully. They're negotiating harder.

But don't panic. Nashville still has strong fundamentals. Homes are selling. You just need the right approach.

Price It Right, Sweeten the Deal, Sell Faster

Competitive Pricing from Day One

Overpricing kills momentum fast. Buyers see your overpriced listing. They pass it by. It sits. After a few weeks, buyers wonder what's wrong with it. You end up cutting the price anyway, but now you've lost the best buyers and wasted valuable time.

Back when buyers were scrambling to lock in low rates, you might have been able to get away with an over-market price. Now, when buyer budgets are already squeezed with higher payments? Not a chance. Today's buyers are extremely budget-conscious.

Work with an agent who knows your specific Nashville neighborhood. Don't price based on what your neighbor got in 2022. That was a different market. Base your asking price on comparable homes in your area that sold in the last 60–90 days at current rates.

Price competitively from day one. You'll attract more showings, more offers, and sell faster.

Offer Buyer Incentives

Closing cost assistance is becoming more common in Nashville. You can also offer rate buydowns. This is where you pay money at closing to reduce the buyer's interest rate. A 1% buydown will cost you a few thousand, but it could be the difference between getting an offer or not.

This is especially important when you’re selling to a first-time homebuyer. Without equity from a previous home sale, first-time buyers are especially receptive to anything that reduces their initial buying costs.

Home warranties give buyers peace of mind about appliances and systems. Repair allowances let buyers fix things their way rather than negotiating every small issue during inspection.

These incentives cost you money, but they sell homes faster. A faster sale often nets you more money than sitting on the market for months.

Make It Move-In Ready

First impressions matter more when buyers are nervous about monthly payments. They don't want to see a fixer-upper that needs $20,000 in immediate out-of-pocket repairs.

Smart home features attract millennial buyers, who make up a huge portion of the market. A smart thermostat, doorbell camera, and security system aren't expensive in the grand scheme of things but signal a modern, updated home.

Energy-efficient upgrades appeal to Nashville buyers worried about rising utility costs. New windows, updated HVAC, and better insulation lower monthly operating costs, which helps offset higher mortgage payments.

Professional staging helps buyers visualize living in your space. It feels counterintuitive, but empty rooms look smaller. Cluttered rooms look messy. Staged rooms look aspirational. Staged listing photos get more attention and help you sell faster.

Be Flexible on Terms

Adjust closing timelines to match buyer needs. Some need 60 days to sell their current home. Others want to close in 30 days. Being flexible attracts more offers.

Be open to negotiation on inspection items. In today's market, buyers expect sellers to address reasonable repair requests. Don't dig in your heels over $500 worth of fixes when it could cost you the sale.

For informational purposes only. Always consult with a licensed mortgage or home loan professional before proceeding with any real estate transaction.

Your Next Steps in Nashville's Market

Interest rates change the game. 6% rates are a reality for 2026, and the high borrowing costs compared to recent years are affecting both buyers and sellers.

But Nashville's real estate market is still active, homes are still selling, and buyers are still finding properties they love. You just need the right strategy and realistic expectations.

If the opportunities of Nashville excite you, contact The Ashton Real Estate Group of RE/MAX Advantage with Nashville's MLS at (615) 603-3602 to get in touch with local real estate agents who can help find the perfect Nashville home for you today.